Still faced with a structural deleveraging in personal and

public debt, the policy response by those who ought to know better remains the

same – juice the system and hope growth miraculously appears. That’s right, the same strategy as adopted

for Greece, Portugal, Spain, France etc, etc, & etc.

After the >+10% MoM rise in asking prices for London homes

published by Rightmove, another vested interest group, the Council for Mortgage

Lenders issued a press release highlighting the increase in mortgage approvals from

64k in August to 67k in September. Bank of England data released on 18 October

was already showing a 25% YoY increase in UK property backed loans for

August. Consumer credit meanwhile is

not being restricted to just property backed loans. The Arch-Bishop of Canterbury may not approve,

but net unsecured debt is also up, rising by £411m MoM in September; a +4.4%

YoY increase. As good Keynsians know well, rising credit

equates to increased consumption and therefore growth so all this must be good

for the recovery!

Encouraging consumers to leverage into property ahead of a

possible rise in interest rates or take on more Wonga type debt however, seems

an odd basis for celebration if not supported by real income growth. Consumer credit may be expanding to fund

current consumption, but real income growth will need to be supported by

re-investment by industry. While

consumers were loading up with £411m of additional unsecured credit in

September, lending to SMEs fell by an almost comparable amount of -£383m. You can’t blame the banks as they are merely

responding to the environment that Governments and regulators have created,

just as we saw with most other financial cock-ups from the Savings and Loans

debacle to the sub-prime crash. When you

can make a property loan with a Government backed guarantee or a pay-day loan

with an APR of >1000%, then why should a bank go at risk to lend to some SME

with no realisable assets and a business plan you don’t understand?

Property back loans continue to rise: +67k in Sept vs +64k

in Aug

Consumer credit increases +£411m in September

SME lending however down £383m in September

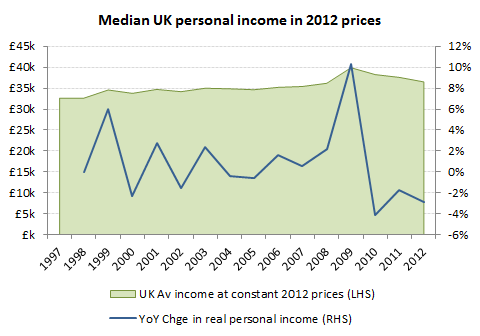

Not exactly positive for real personal income growth!

Consumers therefore continuing to buy more stuff with cheap

credit, but particularly vulnerable to any increase in debt servicing costs

while real income growth and SME investment remain constrained.