Once upon a time, small and impoverished countries could still enjoy top quality TV programmes, even if it meant having to acquire most of them from abroad. This was because the value of these secondary rights reflected these countries capacity to pay and the basis on which the programme rights were sold and bought; by country. To those wishing to bring about an integrated Eurostate however, this is tantamount to heresy. Fresh from their success from the one-size fits all Euro, we now have the ECJ attempting to legislate from the bench by issuing guidance in the cases of FAPL v QC Leisure and Karen Murphy v Media Protection Services Ltd. (cases C-403/08 and C-429/08) that broadcasters such as BSkyB can no longer expect to have their "exclusive" territorial rights protected from cheap parallel imports.

http://curia.europa.eu/jcms/upload/docs/application/pdf/2011-10/cp110102en.pdf

At first sight this might seem like a victory for the 'consumer' by enabling them to acquire the cheapest content anywhere within the EU. For those with cheap broadcasting rights in small countries, this must seem like a licence to print money. Freed from their contractual obligations not to re-distribute rights outside their exclusive territories, the ECJ guidance would now legalise the the arbitrage of hitherto locally licenced rights across the whole EU market. The key focus of the ECJ guidance relates to live rights that are not covered by copyright and the re-sale of the rights to commercial users such as pubs and clubs where BSkyB generates over £200m pa of marginal revenues. The limited adverse reaction in the BSkyB share price on this news however suggests that markets are not overly concerned by the apparent challenge, and perhaps with some justification.

So what does the ECJ guidance actually say?

1) "In its judgment delivered today, the Court of Justice holds that National legislation which prohibits the import, sale or use of foreign decoder cards is contrary to the freedom to provide services and cannot be justified either in light of the objective of protecting intellectual property rights or by the objective of encouraging the public to attend football stadiums."

- a fairly clear validation of Karen Murphy's (and other Pub & Club owners) use of cheaper offerings of Premier League content from Greece (Nova) which were around a tenth the price of Sky's.

2) "So far as concerns the possibility of justifying that restriction in light of the objective of protecting intellectual property rights, the Court observes that the FAPL cannot claim copyright in the Premier League matches themselves, as those sporting events cannot be considered to be an author’s own intellectual creation and, therefore, to be ‘works’ for the purposes of copyright in the European Union."

- a cast of actors kicking a football around a pitch would therefore be a protected work of copyright. How this differs from many PL football matches though is a mystery to me! In the meantime a few clever lawyers will no doubt recommend that Sky includes a major work of copyright in its live transmission feeds to overseas rights holders such as its logo, which would provide it with copyright protection.

3) "Also, even if national law were to confer comparable protection upon sporting events – which would, in principle, be compatible with EU law – a prohibition on using foreign decoder cards would go beyond what is necessary to ensure appropriate remuneration for the holders of the rights concerned."

I believe the translation would be "not so fast eenglish! We don't care what clever legal trick you pull, you're still going to have to compete with cheap Greek decoders and services." In other words, although the ECJ is offering guidance on what it deems non-copyright live broadcasts, the principle can and will be extended to copyrighted works if this is what it takes to establish a pan-european market. The veil slips further with regards the ECJ's underlying political agenda with is subsequent comments

4) "payment by the television stations of a premium in order to ensure themselves absolute territorial exclusivity goes beyond what is necessary to ensure the right holders appropriate remuneration, because such a practice may result in artificial price differences between the partitioned national markets. Such partitioning and such an artificial price difference are irreconcilable with the fundamental aim of the Treaty, which is completion of the internal market.

For similar reason the system of exclusive licences is also contrary to European Union competition law if the licence agreements prohibit the supply of decoder cards to television viewers who wish to watch the broadcasts outside the Member State for which the licence is granted"

- the real agenda, remove these internal "partitioning", notwithstanding that they reflect the inconvenient fact that there is not even a common language.

Perhaps the ECJ is courting Murphy's law here, or just the law of unintended consequences. As with the Euro experiment, the initial benefit to Greek rights holders, may prove less advantageous with time. Will the FAPL really risk its >£600m pa UK TV rights for the <£120m pa that it receives from the whole of the rest of Europe? If it can only sell exclusive rights across all of Europe, rather than nationally, then that is surely what it will do. In this circumstance, what chance will Nova get in securing the current low price it pays for the PLFA games? The hard truth is that audiences in small markets such a Greece benefit enormously from separate local markets for content. By encouraging Greek rights holders to arbitrage this content into richer markets (in contravention of their contractual obligations they agreed to when they secured these rights in the first place) may provide a short term revenue advantage, but at considerable longer term risk as these contracts renew. For larger operators, such as BSkyB, the ECJ's guidance might actually result in a greater concentration of rights ownership and subscribers. If this is not what the ECJ intends, it may be forced to further restrict the ability of rights holders to sell exclusive rights, and therefore fundamentally impair content valuations across the EU.

Tuesday, 4 October 2011

Wednesday, 13 July 2011

BSkyB - look beyond the lynch mob

So the lynch mob is out and led by such political worthies as Keith Vaz. How can David Cameron do anything else but embrace the 'popular' frenzy that has been whipped up by Murdoch's media rivals and fickle Westminster toadies. The BSkyB bid is of course now dead, or so we are reliably informed by Roland Rat's creator and as MPs exercise some political posturing by voting against the deal (albeit legally meaningless), prior to jetting off on vacation to exotic locations on taxpayer funded junkets or courtesy of some dodgy billionaire sponsor.

Naturally Murdoch will be suitably humbled and slink off to the US, never to grace these shores again. Dream on!

As Murdoch's shares free-fall, what are the options for BSkyB's share and how should investors position themselves.

Option 1: Murdoch/News Corp is not deemed fit and proper to own a UK broadcaster. While an unlikely verdict by OFCOM, it could precipitate either Murdoch withdrawing from News Corp's management or a sale of their current 39% holding in BSkyB (as this already represents a controlling interest). Both outcomes could be positive by either reviving the bid or forcing News Corp to divest. To seek the best possible price for shareholders, News Corp would undoubtedly use its controlling stake to put BSkyB into play to secure a control premium for its shares.

Option 2: Status Quo - Murdoch/News Corp remain fit to own BSkyB, but are scared off from pursuing the bid or are blocked by a spurious 'public interest' test (which could be appealed) and sit still with their existing stake until the storm passes. Without the immediate bid premium, the shares settle down to a fundamental valuation, although as highlighted by my FCF/Growth rating analysis, as margins ratchet up, this may not be materially below were they are at the moment.

Option 3: Murdoch fights back - Today's fight-back from the Sun and Times suggest that there may be life in the old dog and that he's not going to give up his bone just yet. The general assumption that top management is implicated in illegal activities has yet to be proved. While the concession to having the bid referred to the competition authority (by withdrawing the earlier concession to divest Sky News) will kick the deal into touch for a good six months, it would provide Murdoch more time to resolve some News Intl management issues as well as get his PR response to these accusations better sorted.

For premium research content including bespoke analysis and valuations please contact me at adelarrinaga@gmail.com for further information

Monday, 11 July 2011

BSkyB valuation trade off between growth and margins

Rebekah Brooks may have described the News of the World as being toxic, although one might well ask under whose watch this originated. Murdoch's desperate attempts to distance himself and News Corps bid for BSkyB from the phone tapping (and worse) scandal by discarding the offending title, but retaining her however risks all of this. Not only has it failed to end the media feeding frenzy, but it has also scared the government into delaying a decision on the bid and even resulted in dark mutterings from OFCOM about reviewing News Corps fitness to own Sky at all.

With a delay and possible challenge to the bid, the BSkyB shares dropped to only 750p on Friday, a level halfway between the original 700p per share offer and the >800p that the independent directors indicated would be the minimum necessary to secure their support. Having sacrificed the UK's largest paid circulation title (and > 200 staff) to stay in with a chance at Sky, will Murdoch's sense of personal loyalty to Rebekah be allowed to stand in the way of this, particularly if she's off David Cameron's Christmas card list? BSkyB's short term share price performance may therefore be inversely proportional to the length of her continued tenure, which may not be long.

Beyond the hysteria, markets will need to keep an eye on what Sky may be worth. Still in investment mode, the group has traded margins for growth, which naturally makes the stock look expensive on near term metrics. However, the group is past an investment inflection point and leveraging its dominant market position, control of content and rising subscriber and revenue base this is changing rapidly. Current EBITA margins are sub 20%, but these are capable of rising to the mid-twenties while still supporting near market average growth rates. Looking at the valuation in terms of a low-twenties normalised margin and even sub market growth rates of +3.5-4.5% CAGR could comfortably support a valuation of between 800-900p per share on my growth model. Squeeze the margins up a little to mid-twenties and the growth rating to a still sub-market growth rate of +5% and one can quickly see how some major shareholders have been arguing for a price of around £11 per share.

BSkyB - valuation trade off between growth and margins

With a delay and possible challenge to the bid, the BSkyB shares dropped to only 750p on Friday, a level halfway between the original 700p per share offer and the >800p that the independent directors indicated would be the minimum necessary to secure their support. Having sacrificed the UK's largest paid circulation title (and > 200 staff) to stay in with a chance at Sky, will Murdoch's sense of personal loyalty to Rebekah be allowed to stand in the way of this, particularly if she's off David Cameron's Christmas card list? BSkyB's short term share price performance may therefore be inversely proportional to the length of her continued tenure, which may not be long.

Beyond the hysteria, markets will need to keep an eye on what Sky may be worth. Still in investment mode, the group has traded margins for growth, which naturally makes the stock look expensive on near term metrics. However, the group is past an investment inflection point and leveraging its dominant market position, control of content and rising subscriber and revenue base this is changing rapidly. Current EBITA margins are sub 20%, but these are capable of rising to the mid-twenties while still supporting near market average growth rates. Looking at the valuation in terms of a low-twenties normalised margin and even sub market growth rates of +3.5-4.5% CAGR could comfortably support a valuation of between 800-900p per share on my growth model. Squeeze the margins up a little to mid-twenties and the growth rating to a still sub-market growth rate of +5% and one can quickly see how some major shareholders have been arguing for a price of around £11 per share.

BSkyB - valuation trade off between growth and margins

Although a >+5% CAGR growth rating may be an ambitious expectation on current consensus revenue growth forecasts beyond 2013, the group has sustained a growth rating in excess of this in all but two years, 2005 and 2006, when I estimate it fell to +3.6% and +2.8% respectively.

For premium research content including bespoke analysis and valuations please contact me at adelarrinaga@gmail.com for further information

Thursday, 7 July 2011

News of the World - Will amputation save the patient (bid)

"Murdoch shutters the venerable 'News of the Screws'" Was this an act of contrition for the phone tapping scandal or an act of desperation to secure regulatory (read political) approval for News Corporations bid for the outstanding shares in BSkyB? If so, will it work when the editor of the NoW at the time of these infractions remains in place at the top of the corporate pole, yet the rest are sacrificed?

As an attempt to draw a line under the phone hacking scandal, this rather radical action is unlikely to satisfy the 'liberal' media. Much of their real gripe had less to do with their sense of moral indignation of phone tapping, than their concern about Murdoch's bid for the rest of BSkyB. However, this action tells us a lot about Murdoch's determination to secure his real prize of BSkyB and this is unlikely to be missed by markets. Existing BSkyB shareholders meanwhile will no doubt have their resolve harden to hold out for a knockout price.

When Murdoch waves goodbye to the News of the World and 200 staff, will he really abandon its 7.5m readers, 2.6m of weekly sales and annual revenues approaching £200m (including approx £110m from copy sales)? Rumours had already been circulating that News Intl was looking to move to a 7 days a week operation to offset the structural decay in readership and revenues. In this case, keeping the captain while throwing the crew overboard makes a lot of sense.

As an attempt to draw a line under the phone hacking scandal, this rather radical action is unlikely to satisfy the 'liberal' media. Much of their real gripe had less to do with their sense of moral indignation of phone tapping, than their concern about Murdoch's bid for the rest of BSkyB. However, this action tells us a lot about Murdoch's determination to secure his real prize of BSkyB and this is unlikely to be missed by markets. Existing BSkyB shareholders meanwhile will no doubt have their resolve harden to hold out for a knockout price.

When Murdoch waves goodbye to the News of the World and 200 staff, will he really abandon its 7.5m readers, 2.6m of weekly sales and annual revenues approaching £200m (including approx £110m from copy sales)? Rumours had already been circulating that News Intl was looking to move to a 7 days a week operation to offset the structural decay in readership and revenues. In this case, keeping the captain while throwing the crew overboard makes a lot of sense.

If News Intl is really going to abandon the Sunday market, the main beneficiary would be Trinity Mirror, with its two ailing titles, the Sunday Mirror and People. However, I suspect that the bounce in its share price on this expectation may be fairly muted as markets see through the ruse. In a sense, Murdoch may be trying to kill two birds with one stone here. Lance a story that was threatening his bid for BSkyB while accelerating a cost reduction plan for his newspapers. 200 angry journalists and hardened price expectations by BSkyB shareholders however might provide an offsetting price to pay.

Tuesday, 28 June 2011

Healthcare information assets still hot

Hot on the heals of Thomson announcing its intention to sell its Healthcare operations, which primarily service US healthcare payers with infomation services to manage the ever spiralling costs of healthcare, Experian has today reported a purchase in the same space, albeit of a considerably smaller operation.

Experian is paying $185m for Medical Present Value (MPV) which maintains a data-base of health claims and provides products to establish patients eligibility for insurance and other financial support and supplements a segment that Experian initially entered only back in 2008.

http://production.investis.com/experian/rns_news/rnsitem?id=4321055

Not much financial information on the subscription based MPV has been provided beyond a 3-year compound revenue growth reported at +30%, and prospective revenues and EBIT of $45m and >$10m respectively (therefore >22% margins and slightly ahead of Thomson Healthcare). On a year-1 basis, MPV is therefore priced at an aggressive >4x revenues and >18x EBIT (5.5% yield), on which basis Experian expects MPV to be EPS accretive. Including similar assumptions for cash conversion (of 90%) and tax (at 30%) as I used for Experian and the Y1 FCF yield of under 3.5%. Clearly Experian will be looking for cost synergies with existing activities as well as a network effect on revenues to raise this to its own FCF yield of over 5%. Another couple of years of 20% compound growth should do the trick!

While Experian will face the task of convincing its shareholders of the maths, the deal however should assist Thomson in its own valuation expectations for its healthcare assets and where a 5% current year FCF yield would support a gross price of around $1.4bn and comfortably over $1bn after tax.

Experian is paying $185m for Medical Present Value (MPV) which maintains a data-base of health claims and provides products to establish patients eligibility for insurance and other financial support and supplements a segment that Experian initially entered only back in 2008.

http://production.investis.com/experian/rns_news/rnsitem?id=4321055

Not much financial information on the subscription based MPV has been provided beyond a 3-year compound revenue growth reported at +30%, and prospective revenues and EBIT of $45m and >$10m respectively (therefore >22% margins and slightly ahead of Thomson Healthcare). On a year-1 basis, MPV is therefore priced at an aggressive >4x revenues and >18x EBIT (5.5% yield), on which basis Experian expects MPV to be EPS accretive. Including similar assumptions for cash conversion (of 90%) and tax (at 30%) as I used for Experian and the Y1 FCF yield of under 3.5%. Clearly Experian will be looking for cost synergies with existing activities as well as a network effect on revenues to raise this to its own FCF yield of over 5%. Another couple of years of 20% compound growth should do the trick!

While Experian will face the task of convincing its shareholders of the maths, the deal however should assist Thomson in its own valuation expectations for its healthcare assets and where a 5% current year FCF yield would support a gross price of around $1.4bn and comfortably over $1bn after tax.

Another example of how legacy print media valuations have tanked

David Levin's long term re-structuring of UBM to exit its declining legacy print businesses continues. Yesterday UBM announced that it is selling its UK entertainment and technology portfolio (including Music Week and Pro Sound News) to Intent Media. In itself, there is little of surprise as UBM exits this small segment which represented less than 4% of its print magazine revenues last year and will gain some additional scale benefits in the sector from Intent (albeit only modestly). Of interest however is the miserable price achieved of only £2.4m. This represents an exit multiple of under 50% of the portfolio's sales last year (of £5.4m) and 4x EBITA (of c. £0.6m). What is not revealed however, is the prospective liabilities being assumed by Intent (including redundancies and possibly pensions etc) to offset what would appear to be a deal generating an initial EBITA return of around 25%.

Impact on UBM's valuation? Another example of the need to look through to see where the profits come from rather than the overall figure. While the multiple of sales of under 50% is similar to the level at which I already value UBM's print magazine interests (from a normalised FCF yield basis) it may provide a wake-up call to those who have valued the business on an overall PE basis, which anyway is already flattered by the treatment of the tax assets and low tax charge recognised through the P&L.

UBM valuation

Impact on UBM's valuation? Another example of the need to look through to see where the profits come from rather than the overall figure. While the multiple of sales of under 50% is similar to the level at which I already value UBM's print magazine interests (from a normalised FCF yield basis) it may provide a wake-up call to those who have valued the business on an overall PE basis, which anyway is already flattered by the treatment of the tax assets and low tax charge recognised through the P&L.

UBM valuation

Thomson Reuters - another divestment, but what to do with the cash?

Unless one wants to lend to one of the PIIGS, cash returns are currently too low to tempt corporates to sit on excess cash. But what to do with it? For Thomson Reuters this issue will become increasingly pertinent following its announcement to divest its healthcare operations (c. $500m of sales and $100m of EBITA) which I estimate could generate a further $1.2bn on net proceeds in addition to the c. $1bn already raised from the disposal of peripheral assets across Legal and Markets divisions (of BAR BRI, Scandinavian Legal & Tax businesses, Risk and Portia businesses). By the end of 2011, net debt therefore could fall to below $4bn (from $6.4bn), which with $6.6bn of term debt could see gross cash of over $2.5bn sitting on the balance sheet and diluting EPS. With $2.5bn of un-utilised bank facilities this could provide the group with a potential funding headroom (under existing funding arrangements of over $5bn.

For a subscription based professional publisher, a 2-3x net debt to EBITA ratio is a comfortable level of financial leverage and indeed, broadly reflects the average levels sustained by the sector over the past 20 years. While the issue of under-leverage will not be unique for Thomson Reuters after this year, a debt to EBITA ratio of below 1.0x and the sizable gross cash position will exert pressure on management to allocate this into more productive areas. In the past, management has not shied away from taking bold steps to refocus the portfolio (Reuters being a case in point) and has also instigated share buy-back programmes to soak up excess capital. Since the $17bn acquisition of Reuters in 2008 however, the group has been relatively inactive in applying its circa $1.5bn pa of FCF (I estimate $1.8bn for 2011 and $2.4bn for 2012), with only $349m of acquisition spend and $905m of dividends in 2009, rising to $612m and $898m respectively for 2010. For 2011 the group has continued to focus its acquisition strategy on smaller infill purchases such as Manatron (property tax software for Governments), Mastersaf Brazil (Brazil legal publisher) and World-Check (personal & corporate risk information) and has not yet signalled an appetite for something more substantial. The disposal strategy meanwhile seems to aim at discarding peripheral activities, even if currently performing strongly. Healthcare, which has been exploiting the rising demand for 3rd party payer services in the US appears another example, delivering robust growth, but with a US market model that may have more limited applications elsewhere.

Excess liquidity with prospective cash of >$2bn and a further $2.5bn of undrawn facilities

For a subscription based professional publisher, a 2-3x net debt to EBITA ratio is a comfortable level of financial leverage and indeed, broadly reflects the average levels sustained by the sector over the past 20 years. While the issue of under-leverage will not be unique for Thomson Reuters after this year, a debt to EBITA ratio of below 1.0x and the sizable gross cash position will exert pressure on management to allocate this into more productive areas. In the past, management has not shied away from taking bold steps to refocus the portfolio (Reuters being a case in point) and has also instigated share buy-back programmes to soak up excess capital. Since the $17bn acquisition of Reuters in 2008 however, the group has been relatively inactive in applying its circa $1.5bn pa of FCF (I estimate $1.8bn for 2011 and $2.4bn for 2012), with only $349m of acquisition spend and $905m of dividends in 2009, rising to $612m and $898m respectively for 2010. For 2011 the group has continued to focus its acquisition strategy on smaller infill purchases such as Manatron (property tax software for Governments), Mastersaf Brazil (Brazil legal publisher) and World-Check (personal & corporate risk information) and has not yet signalled an appetite for something more substantial. The disposal strategy meanwhile seems to aim at discarding peripheral activities, even if currently performing strongly. Healthcare, which has been exploiting the rising demand for 3rd party payer services in the US appears another example, delivering robust growth, but with a US market model that may have more limited applications elsewhere.

A $2bn buy-back would be a low-risk option

Thomson Reuters may not be the highest yielding media opportunity around, but a share buyback to utilise say $2bn of prospective excess cash would provide a low risk option to offset the EPS dilutive impact of this year's divestments, while representing a 7% reduction in in the equity base. At current levels I estimate that the group trades on an operating FCF yield of 6% for FY11, rising to almost 7% for next year. Grossing up for assumed tax at 30%, this represents an EBITA yield of over 8.5% for FY11 and 9.7% for FY12.

Thomson Reuters may not be the highest yielding media opportunity around, but a share buyback to utilise say $2bn of prospective excess cash would provide a low risk option to offset the EPS dilutive impact of this year's divestments, while representing a 7% reduction in in the equity base. At current levels I estimate that the group trades on an operating FCF yield of 6% for FY11, rising to almost 7% for next year. Grossing up for assumed tax at 30%, this represents an EBITA yield of over 8.5% for FY11 and 9.7% for FY12.

Would Thomson use its $5bn of funding headroom to launch a more sizable bid for either an existing competitor (eg Reed Elsevier or Wolters Kluwer) or to leverage a platform into an adjacent area such as risk information? This certainly remains a possibility and rival valuations are not particularly demanding. Choice assets such as Wolters Kluwer's CCH tax and accounting business or its compliance or European legal content however could also trigger regulatory investigation which might restrict Thomson's scope for manoeuvre. For the present, I would expect Thomson to continue its policy of infill acquisition of niche content and software, particularly across legal and tax and in emerging markets which can be folded into its existing distribution and technology platform. As such, the recent divestments ought not to be interpreted as prelude to a major acquisition with its accompanying risk of value dilution. While selling businesses on EBITA yields of perhaps 7% (and FCF yields of around 5%) for a cash interest return of possibly less than 2% will have an initially dilutive impact to EPS forecasts, this could be more than offset by a share buyback.

Thomson Reuters valuation range +5.5-6.5% CAGR = U$37-45 ps

Underlying Legal and Financial markets are still struggling to find direction while the initial dilution from the divestments are also capping the momentum in EPS forecasts for Thomson. As a consequence, Thomson's growth rating has stalled within a narrow growth rating range of approx +5% to +5.5%. While subscription lag is seeing current organic revenues are lagging this rate of growth, a rising trend of net new sales based on a well invested pipeline of new services, market leadership and supported by pricing power could see organic revenues exceed this growth rating by next year. As revenue momentum recovers there should be scope to see the growth rating return to a +5.5% to +6.5% growth rating range again which would equate to an NPV of around U$37-45 ps.

Summary valuation

Friday, 24 June 2011

Groupon - marketing services, group buying middleman or loan shark?

The bottom line is that investors will have to take a massive leap of faith to get anywhere near the $20-25bn MV estimates that seem to floating around. And this doesn't even include their aim to disenfranchise new equity by offering non-voting shares or the potential bad debt problem that could emerge from the explosive geographical expansion and inherent business model.

As a piece of financial engineering, Groupon's model is interesting, although not without risk. When I initially looked at Groupon I thought it might be a cross between a marketing services business (providing promotional services to local merchants) and a group buying middle man. From the perspective of some local merchants however, Groupon may also be seen as a lender of last resort to ailing traders. Notwithstanding Groupon's negative working capital characteristics (paying merchants in stages up to 60 days after selling a Groupon), merchants may also end up receiving cash ahead of actually having to deliver on the Groupon obligation. For a Merchant in a cashflow crisis therefore, a Groupon could offer a merchant a quick cash injection, albeit at exorbitant rates. If one looks at Groupon from this perspective, it could be a lender of last resort, but at loan shark rates of 100% plus (with Groupon keeping 50% of the face value of the Groupon).

This might also lead to an adverse selection problem of a deteriorating customer profile as the weaker the merchant, the more likely they need new customers and financing on these terms. It is not clear whether unscrupulous merchants have learnt to game the system yet, but accrued merchant payables are already at over $291m (as at March) and the pace of expansion could well open up a significant bad debt problem that the negative working capital position would help to disguise so long as they keep growing. Should growth stall however, it could all look very messy indeed!

Perhaps the Greeks could use a few of these Groupons

As a piece of financial engineering, Groupon's model is interesting, although not without risk. When I initially looked at Groupon I thought it might be a cross between a marketing services business (providing promotional services to local merchants) and a group buying middle man. From the perspective of some local merchants however, Groupon may also be seen as a lender of last resort to ailing traders. Notwithstanding Groupon's negative working capital characteristics (paying merchants in stages up to 60 days after selling a Groupon), merchants may also end up receiving cash ahead of actually having to deliver on the Groupon obligation. For a Merchant in a cashflow crisis therefore, a Groupon could offer a merchant a quick cash injection, albeit at exorbitant rates. If one looks at Groupon from this perspective, it could be a lender of last resort, but at loan shark rates of 100% plus (with Groupon keeping 50% of the face value of the Groupon).

This might also lead to an adverse selection problem of a deteriorating customer profile as the weaker the merchant, the more likely they need new customers and financing on these terms. It is not clear whether unscrupulous merchants have learnt to game the system yet, but accrued merchant payables are already at over $291m (as at March) and the pace of expansion could well open up a significant bad debt problem that the negative working capital position would help to disguise so long as they keep growing. Should growth stall however, it could all look very messy indeed!

Perhaps the Greeks could use a few of these Groupons

Tuesday, 21 June 2011

Groupon in need of a Groupon

Good to see that markets have a handle on valuing the current batch of internet IPO's. Having initially more than doubled from its listing price, Linkedin's subsequent -35% share price retrenchment means that it is now only 47% ahead on its original offer price last month. Pandora meanwhile also seemed be getting off to a good start with an initial rise of +25%, although the subsequent -50% fall meant that it ended its big day down -35%. But then Pandora is not 'Social Media' and we've all heard that social media is hot, or at least as long as one isn't trying to sell off MySpace! So what about Groupon, that almost social media group buying network, but with explosive growth that is limbering up for its own IPO?

As with all these embryonic dotcoms, one is being asked to buy into a longer term story that has yet to be fully formulated and where even current data on key metrics, such as merchant retention and customer churn, are not available. Groupon's current performance provides evidence that, so far at least, the model works as an effective promotional tool for local merchants as well as Groupon's ability to negotiate a sizable share (50%) of the discount (>50%) offered to customers that it is able to reach. The merchant however retains less than 25% of the full ticket price of the service under the offer, which means that unless it carried an original gross margin of over 75%, the viability of a Groupon as a sustainable marketing tool will hinge on whether it builds repeat customers at full price. A deeply discounted Groupon clearly builds sampling, but the evidence on customer loyalty and merchant retention is more patchy. For the present, this does not appear to have adversely impacted Groupon's ability to sign up merchants or to squeeze gross margins or average customer spend as the competitive challenge has emanated mainly from hundreds of daily-deal Groupon clones such as LivingSocial. The entry of tech and data rich internet networks such as Google, Facebook and Microsoft into this space however, could start to change these dynamics as they leverage their social media and user data to offer relevancy and loyalty tools to merchants. As the competition broadens the value proposition into these areas, will this commoditise those daily-deals sites stranded with a relatively narrow value proposition of offering a discount to an email distribution list? If you think so, then the trajectory for prospective gross margins and customer value may struggle to justify the pre-listing spin of an IPO valuation perhaps topping $20bn.

Quick & Dirty valuation

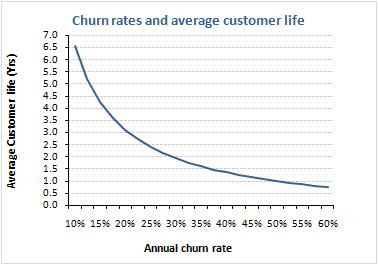

In its S-1 pre-listing teaser Groupon omitted to include some important metrics on areas such as customer churn and merchant retention which would have provided a better steer on customer life time value (CLTV), customer acquisition costs and therefore the basis for a per customer valuation. A metric which Groupon is choosing to highlight however is something referred to as 'CSOI' (consolidated segment operating income), which excludes marketing and stock compensation charges. While stock compensation should be regarded as a real expensable cost, a pre marketing EBITA can be used to provide some sort valuation perspective; albeit one still needs to make a stab at a normalised marketing spend per subscriber and a churn assumption to estimate the period over which this ought to be amortised. For Q1 FY11, reported CSOI excluding stock comp was $63m or an annualised $16 per customer. Adjusting for the step up infrastructure spend in SG&A in Q1 and some prospective scale benefits, this might suggest adjusted CSOI of perhaps $20-25 per customer pa. At $208m, Q1 marketing costs represented an annualised charge of over $50 per customer, although assuming a 20-30% reduction for future scale efficiencies and an abnormally heavy weighting in Q1 from Groupon's race for leadership, might see this ease back to nearer $35-40 per customer. To breakeven on a per customer basis therefore would need to this figure to be amortised over 1.5-2.0 years and require an underlying customer churn rate of under 35%, if not under 30%. Even spreading customer acquisition expenditure over 5 years (and an approx 12% churn rate) would suggest an underlying EBITA per customer of $12-18. Apply a 5% FCF yield to the upper end of this range (and 14x EBITA assuming a 30% normalised tax rate and 100% cash conversion) and this could suggest a value per customer topping out at around $250. On this basis, markets may need to be looking for 80m customers by year 3 and a quarterly net addition rate over over 5m per quarter to underpin a current EV of over $15bn.

To reach a current market valuation of even $15bn for Groupon may require some aggressive, if not heroic assumptions will need to be made, including an act of faith on future underlying churn. Apply a 3 year valuation horizon and the group will need to be worth at least $20bn at the period end for it to justify $15bn today. Even if Groupon were to add another 20m customers over this period (from 16m currently to 36m) this would require an EV per customer at the period end of over $550. On an operational FCF yield range of 5%-7% (vs >12% for Google and 7% for the market for 2014e) I estimate that the underlying EBITA per customer would need to rise to $36-51 pa on this customer base (and after assuming a 30% normalised 30% tax rate and 100% cash conversion).

EBITA per customer needed to support Yr 3 EV of $20bn

While no pretense at sophistication is being made in the above 'quick & dirty' calculations, they should help to provide a rough framework of some of the issues and assumptions that will need to be considered in formulating a valuation. With Groupon still in 'land grab' mode, attention is understandably focused on the stellar growth being achieved in customers and revenues rather than the low barriers to entry and what may also prove to be modest scale advantages. With underlying growth already maturing in some of the earlier penetrated regions, growth is being increasingly based on the geographical extension of the brand, all of which require their own layer of investment in areas such as sales to support them which might imply a higher level of variable costs and therefore lower rate of operational leverage in the business model than may be assumed in the IPO brouhaha. Using my earlier $15 per customer underlying EBITA estimate ($12-18 range) and 14x EBITA multiple (and 5% FCF yield) on a 36m customer base by 2014, this would suggest an EV of approx $7.5bn or an NPV of nearer $6bn. Not a million miles from Google's offer back in December which was rejected!

Land grab metrics

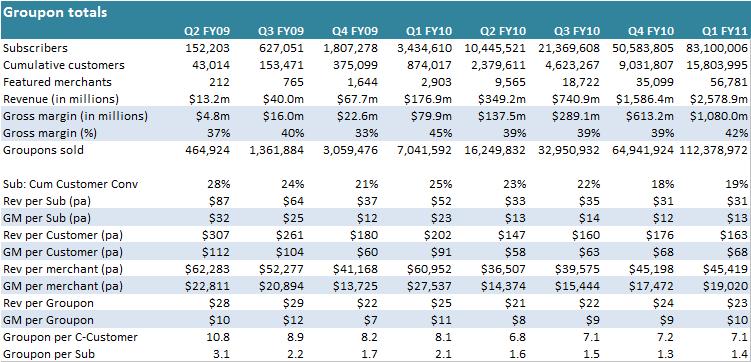

From a standing start to $2.5bn pa of revenues, 16m customers and a footprint across 500 markets in just 30 months is certainly impressive. In this dash for growth and first mover advantage however, it is easy to miss that the group has been increasingly reliant on the geographical extension of its model to drive this growth. In the process, the average conversion of 'subscribers' [those on the email distribution list agreeing to receive offers, rather than actual paying subscribers] to customers is in decline (42% in Q1 FY11 vs 45% in Q1 FY10). As Groupon only releases cumulative customer numbers rather than the more relevant active customers, this conversion ratio is therefore already flattered. Revenue and more importantly gross margin per customer meanwhile are all broadly flat as are average Groupon and merchant margins.

Groupon - quarterly data (annualised)

Unit yield from legacy markets eroding

The original and early roll out regions however are beginning to mature. Absolute growth rates in subscribers, customers and Groupons are still being achieved, but the underlying yields on these are deteriorating. As the customer and merchant base ages, Groupon's yield is eroding. What is less clear is whether this is a natural maturing of the market as new entrants (both customers and merchants) dilute higher spending early adopters or a deterioration in the perceived value proposition by existing customers and merchants after using the service.

Boston

QoQ revenue growth is still averaging approx +27%, but the quality of the underlying metrics are deteriorating. Revenues per subscriber are averaging -5% QoQ and -20% YoY, revenues per customer averaging -7% QoQ and -26% YoY, revenues per merchant averaging -1% QoQ and -23% YoY, revenue per Groupon averaging -6% QoQ and -21% YoY and Groupons per customer averaging -2% QoQ and -7% YoY.

For more on the Boston -

http://blog.yipit.com/2011/06/03/groupon-s-1-reveals-business-model-deteriorating-in-oldest-markets/

Chicago

As the longest standing Groupon region Chicago has exhibited similar trends as Boston with QoQ revenue growth is averaging approx +32%, but the quality of the underlying metrics also deteriorating. Revenues per subscriber are averaging -12% QoQ and -39% YoY, revenues per customer averaging -6% QoQ and -23% YoY, revenues per merchant averaging -7% QoQ and -35% YoY, revenue per Groupon averaging -1% QoQ and -5% YoY and Groupons per customer averaging -5% QoQ and -18% YoY.

Costs

Groupon is currently in a land-grab mode, while a valuation will try and anticipate what the underlying costs will be in a more steady state environment. The rate of top-line growth has been phenomenal, but this has been more than matched by costs and without a clear perspective on churn, prospective investors may struggle to determine whether this has been acquired profitably from the GAAP numbers. Fully expensing SAC costs presents a fairly alarming increase in marketing costs per customer (from $12 in 2009 to $53 for Q1 FY11, annualised) and the rise in SG&A costs per customer also suggest a sizable step-up in fixed infrastructure spend to support the aggressive geographical expansion. In total, GAAP operating costs per customer have trebled from $32 pa to $98 pa.

The challenge on modelling Groupon costs is twofold. What is the variable component to costs and over what period should these be recognised? In the below analysis I've guesstimated that variable costs have edged back from 67% to 63% of costs as some (25%) of the recent increase in marketing costs will have reflected a step-up in infrastructure costs from the extending the regional footprint. On the basis of the last reported results (Q1 FY11), amortising these variable costs over say 2 years (approx 30% customer churn) would therefore suggest an annualised variable costs at approx $31 per customer. Include fixed cost at around $36 and the total annual underlying costs would come in at approx $67 per customer vs the GAAP rate of $98.

Modelling gross margin and costs per customer by churn

NPV per customer

NPV per customer

Applying a $70 per customer average cost (with a 63% variable component) and a 25% customer churn (2.5 Yrs av. life) should deliver an average FCF of approx $13 per customer pa (post tax at 30%). Assuming that the market reaches out beyond the current growth build out to a more steady state environment (in 2014), I estimate that the business could trade within a 5% to 7% operating FCF range (discounting CAGR of +7.5% and +5.5% respectively) and a per customer valuation of $191-$267.

Value per customer by churn and FCF yield

Groupon NPV estimate by customer growth and FCF yield

Appendix : Revenue metric charts

Revenue per subscriber: New regions clearly generate considerably less than the the legacy US ones of Chicago & Boston, although the gap is closing as these latter two erode.

Subscriber to customer conversion: New regions have brought down the average, although this metric is distorted by Groupon only reporting on cumulative, rather than active customer numbers which inevitably flatter the customer numbers for the longer established regions.

Revenue per customer: declines across all reported segments although again this will be in part diluted by reporting only cumulative customers rather than active ones

Groupons per customer: As above for revenues per customer

Revenue per Groupon : Apart from London and briefly Berlin, there is little variance by region; at least those disclosed. Trend however still downward, particularly for Boston & Chicago

Revenue per merchant: Relatively stable overall, but with considerable volatility by region and steep declines recently in Boston & Chicago

As with all these embryonic dotcoms, one is being asked to buy into a longer term story that has yet to be fully formulated and where even current data on key metrics, such as merchant retention and customer churn, are not available. Groupon's current performance provides evidence that, so far at least, the model works as an effective promotional tool for local merchants as well as Groupon's ability to negotiate a sizable share (50%) of the discount (>50%) offered to customers that it is able to reach. The merchant however retains less than 25% of the full ticket price of the service under the offer, which means that unless it carried an original gross margin of over 75%, the viability of a Groupon as a sustainable marketing tool will hinge on whether it builds repeat customers at full price. A deeply discounted Groupon clearly builds sampling, but the evidence on customer loyalty and merchant retention is more patchy. For the present, this does not appear to have adversely impacted Groupon's ability to sign up merchants or to squeeze gross margins or average customer spend as the competitive challenge has emanated mainly from hundreds of daily-deal Groupon clones such as LivingSocial. The entry of tech and data rich internet networks such as Google, Facebook and Microsoft into this space however, could start to change these dynamics as they leverage their social media and user data to offer relevancy and loyalty tools to merchants. As the competition broadens the value proposition into these areas, will this commoditise those daily-deals sites stranded with a relatively narrow value proposition of offering a discount to an email distribution list? If you think so, then the trajectory for prospective gross margins and customer value may struggle to justify the pre-listing spin of an IPO valuation perhaps topping $20bn.

Quick & Dirty valuation

In its S-1 pre-listing teaser Groupon omitted to include some important metrics on areas such as customer churn and merchant retention which would have provided a better steer on customer life time value (CLTV), customer acquisition costs and therefore the basis for a per customer valuation. A metric which Groupon is choosing to highlight however is something referred to as 'CSOI' (consolidated segment operating income), which excludes marketing and stock compensation charges. While stock compensation should be regarded as a real expensable cost, a pre marketing EBITA can be used to provide some sort valuation perspective; albeit one still needs to make a stab at a normalised marketing spend per subscriber and a churn assumption to estimate the period over which this ought to be amortised. For Q1 FY11, reported CSOI excluding stock comp was $63m or an annualised $16 per customer. Adjusting for the step up infrastructure spend in SG&A in Q1 and some prospective scale benefits, this might suggest adjusted CSOI of perhaps $20-25 per customer pa. At $208m, Q1 marketing costs represented an annualised charge of over $50 per customer, although assuming a 20-30% reduction for future scale efficiencies and an abnormally heavy weighting in Q1 from Groupon's race for leadership, might see this ease back to nearer $35-40 per customer. To breakeven on a per customer basis therefore would need to this figure to be amortised over 1.5-2.0 years and require an underlying customer churn rate of under 35%, if not under 30%. Even spreading customer acquisition expenditure over 5 years (and an approx 12% churn rate) would suggest an underlying EBITA per customer of $12-18. Apply a 5% FCF yield to the upper end of this range (and 14x EBITA assuming a 30% normalised tax rate and 100% cash conversion) and this could suggest a value per customer topping out at around $250. On this basis, markets may need to be looking for 80m customers by year 3 and a quarterly net addition rate over over 5m per quarter to underpin a current EV of over $15bn.

To reach a current market valuation of even $15bn for Groupon may require some aggressive, if not heroic assumptions will need to be made, including an act of faith on future underlying churn. Apply a 3 year valuation horizon and the group will need to be worth at least $20bn at the period end for it to justify $15bn today. Even if Groupon were to add another 20m customers over this period (from 16m currently to 36m) this would require an EV per customer at the period end of over $550. On an operational FCF yield range of 5%-7% (vs >12% for Google and 7% for the market for 2014e) I estimate that the underlying EBITA per customer would need to rise to $36-51 pa on this customer base (and after assuming a 30% normalised 30% tax rate and 100% cash conversion).

EBITA per customer needed to support Yr 3 EV of $20bn

While no pretense at sophistication is being made in the above 'quick & dirty' calculations, they should help to provide a rough framework of some of the issues and assumptions that will need to be considered in formulating a valuation. With Groupon still in 'land grab' mode, attention is understandably focused on the stellar growth being achieved in customers and revenues rather than the low barriers to entry and what may also prove to be modest scale advantages. With underlying growth already maturing in some of the earlier penetrated regions, growth is being increasingly based on the geographical extension of the brand, all of which require their own layer of investment in areas such as sales to support them which might imply a higher level of variable costs and therefore lower rate of operational leverage in the business model than may be assumed in the IPO brouhaha. Using my earlier $15 per customer underlying EBITA estimate ($12-18 range) and 14x EBITA multiple (and 5% FCF yield) on a 36m customer base by 2014, this would suggest an EV of approx $7.5bn or an NPV of nearer $6bn. Not a million miles from Google's offer back in December which was rejected!

Land grab metrics

From a standing start to $2.5bn pa of revenues, 16m customers and a footprint across 500 markets in just 30 months is certainly impressive. In this dash for growth and first mover advantage however, it is easy to miss that the group has been increasingly reliant on the geographical extension of its model to drive this growth. In the process, the average conversion of 'subscribers' [those on the email distribution list agreeing to receive offers, rather than actual paying subscribers] to customers is in decline (42% in Q1 FY11 vs 45% in Q1 FY10). As Groupon only releases cumulative customer numbers rather than the more relevant active customers, this conversion ratio is therefore already flattered. Revenue and more importantly gross margin per customer meanwhile are all broadly flat as are average Groupon and merchant margins.

Groupon - quarterly data (annualised)

Unit yield from legacy markets eroding

The original and early roll out regions however are beginning to mature. Absolute growth rates in subscribers, customers and Groupons are still being achieved, but the underlying yields on these are deteriorating. As the customer and merchant base ages, Groupon's yield is eroding. What is less clear is whether this is a natural maturing of the market as new entrants (both customers and merchants) dilute higher spending early adopters or a deterioration in the perceived value proposition by existing customers and merchants after using the service.

Boston

QoQ revenue growth is still averaging approx +27%, but the quality of the underlying metrics are deteriorating. Revenues per subscriber are averaging -5% QoQ and -20% YoY, revenues per customer averaging -7% QoQ and -26% YoY, revenues per merchant averaging -1% QoQ and -23% YoY, revenue per Groupon averaging -6% QoQ and -21% YoY and Groupons per customer averaging -2% QoQ and -7% YoY.

For more on the Boston -

http://blog.yipit.com/2011/06/03/groupon-s-1-reveals-business-model-deteriorating-in-oldest-markets/

Chicago

As the longest standing Groupon region Chicago has exhibited similar trends as Boston with QoQ revenue growth is averaging approx +32%, but the quality of the underlying metrics also deteriorating. Revenues per subscriber are averaging -12% QoQ and -39% YoY, revenues per customer averaging -6% QoQ and -23% YoY, revenues per merchant averaging -7% QoQ and -35% YoY, revenue per Groupon averaging -1% QoQ and -5% YoY and Groupons per customer averaging -5% QoQ and -18% YoY.

Costs

Groupon is currently in a land-grab mode, while a valuation will try and anticipate what the underlying costs will be in a more steady state environment. The rate of top-line growth has been phenomenal, but this has been more than matched by costs and without a clear perspective on churn, prospective investors may struggle to determine whether this has been acquired profitably from the GAAP numbers. Fully expensing SAC costs presents a fairly alarming increase in marketing costs per customer (from $12 in 2009 to $53 for Q1 FY11, annualised) and the rise in SG&A costs per customer also suggest a sizable step-up in fixed infrastructure spend to support the aggressive geographical expansion. In total, GAAP operating costs per customer have trebled from $32 pa to $98 pa.

The challenge on modelling Groupon costs is twofold. What is the variable component to costs and over what period should these be recognised? In the below analysis I've guesstimated that variable costs have edged back from 67% to 63% of costs as some (25%) of the recent increase in marketing costs will have reflected a step-up in infrastructure costs from the extending the regional footprint. On the basis of the last reported results (Q1 FY11), amortising these variable costs over say 2 years (approx 30% customer churn) would therefore suggest an annualised variable costs at approx $31 per customer. Include fixed cost at around $36 and the total annual underlying costs would come in at approx $67 per customer vs the GAAP rate of $98.

Modelling gross margin and costs per customer by churn

NPV per customer

NPV per customer

Applying a $70 per customer average cost (with a 63% variable component) and a 25% customer churn (2.5 Yrs av. life) should deliver an average FCF of approx $13 per customer pa (post tax at 30%). Assuming that the market reaches out beyond the current growth build out to a more steady state environment (in 2014), I estimate that the business could trade within a 5% to 7% operating FCF range (discounting CAGR of +7.5% and +5.5% respectively) and a per customer valuation of $191-$267.

Value per customer by churn and FCF yield

Groupon NPV estimate by customer growth and FCF yield

Appendix : Revenue metric charts

Revenue per subscriber: New regions clearly generate considerably less than the the legacy US ones of Chicago & Boston, although the gap is closing as these latter two erode.

Subscriber to customer conversion: New regions have brought down the average, although this metric is distorted by Groupon only reporting on cumulative, rather than active customer numbers which inevitably flatter the customer numbers for the longer established regions.

Revenue per customer: declines across all reported segments although again this will be in part diluted by reporting only cumulative customers rather than active ones

Groupons per customer: As above for revenues per customer

Revenue per merchant: Relatively stable overall, but with considerable volatility by region and steep declines recently in Boston & Chicago

Sunday, 8 May 2011

Q1 Agencies Postscript

The City narrative on the Q1 results seems predictable enough; a positive underlying revenue momentum which is encouraging managements to raise full year trading expectations and return to acquisition led expansion - a big hurrah for the bankers! Equity markets however are proving a tougher nut to convince, given its broader macro focus and as a consequence consensus forecasts for revenues and earnings are showing little change over the past month; barring some rattled Dentsu estimates of course. Offered the choice of listening to bullish management or an increasingly challenged economic recovery, markets know where to place their bets and agency share prices have tended to under-perform accordingly. While many may wish to celebrate that Mo Greene moment in Pakistan, the domestic outlook remains constrained by rising inflation against falling discretionary income and the prospective end of the QE party.

Agency revenue recovery - so far so good

Rate of revenue recovery into 2011 is easing, albeit by less than the reduction in the comparative tailwind might have suggested. For Q1, average organic revenue growth of around +6.6% YoY was -2.9pts below the +9.5% posted for Q4 2010, notwithstanding a +7.2pts tightening in the prior year quarterly comparative from -6.4% to +0.8%. For Q2 meanwhile, agencies are pointing to rates of YoY organic revenue growth that are not vastly dissimilar to those achieved for Q1, which given the further tightening in prior year comparatives (by 4.9pts) has encouraged management to harden full year growth expectations and more importantly to ease restraints on acquisition spend. Two points of note however is firstly the continued high rate of growth still being achieved from the US (averaging around +7%), notwithstanding deteriorating quarterly GDP and outlook. Secondly, FMCG groups such as P&G and Unilever are maintaining A&P spend ratios, while shifting spend from price promotion to brand building advertising to defend increased pricing (in an attempt to pass on commodity inflation equivalent to -500bps of margins). In the short term this has been positive for agency revenues, although whether this is sustainable may depend on the extent to which this additional brand investment really does convert into pricing power.

Agency organic revenue growth (quarterly YoY)

Pricing power or post trough bounce?

The issue of pricing power in an inflationary (and possibly stagflationary) environment goes to the heart of of the agency value debate. FMCG clients are shifting spend into branding to support price increases and this is being reflected in agency revenues. Does this mean that we are now entering a new period of above market growth for agencies? I wouldn't bet on it. Marketers may be currently upping their brand spend, but they are also focusing on raising their marketing ROI, including raising the digital mix. Over the past decade this process has dismantled the distribution bottlenecks of many legacy media with the consequential squeeze on advertising yields. If this has resulted in global adverting expenditure growth falling short of GDP, then this has still exceeded agency organic revenues. Hopes that the current growth in marketing investment and agency revenues represents a paradigm shift therefore seems to be wide of the mark. Structurally, legacy media continues to be disintermediated and agency gross margins remain under pressure. Where gains are made in either organic revenue growth or EBITA margins, this often has as much to do with agencies heavy reliance on acquisition to buy new marketing skills and to shed overlapping costs rather than any fundamental evolution in the agency model. If agencies have been spending over two-thirds of their cash flow to acquire skills, one presumes, in faster growth segments, but still deliver organic revenue growth averaging over -100bps pa less than GDP, then what does this really say above their underlying pricing power. While the riposte may be that much of this performance shortfall is recouped by an average +50bps pa of EBITA margin gain, this conveniently ignores any expensing of acquired intangibles which are consumed. Consider the numbers. Even if these intangibles are consumed and amortised over 20 years, this 5% expense on the two-thirds of FCF spent on acquisitions would therefore equate to -3.3% pa of overall FCF, which is just happens to fully absorb the positive benefits of a +50bps pa EBITA margin increase on a 15% margin base. Using the current recovery in expenditure and revenues to justify a resumption of the acquisition led growth model for agencies therefore represents a somewhat bitter-sweet dilemma for the markets, which probably helps explain the muted response to all the positive trading spin we've been getting.

Agency revenue recovery - so far so good

Rate of revenue recovery into 2011 is easing, albeit by less than the reduction in the comparative tailwind might have suggested. For Q1, average organic revenue growth of around +6.6% YoY was -2.9pts below the +9.5% posted for Q4 2010, notwithstanding a +7.2pts tightening in the prior year quarterly comparative from -6.4% to +0.8%. For Q2 meanwhile, agencies are pointing to rates of YoY organic revenue growth that are not vastly dissimilar to those achieved for Q1, which given the further tightening in prior year comparatives (by 4.9pts) has encouraged management to harden full year growth expectations and more importantly to ease restraints on acquisition spend. Two points of note however is firstly the continued high rate of growth still being achieved from the US (averaging around +7%), notwithstanding deteriorating quarterly GDP and outlook. Secondly, FMCG groups such as P&G and Unilever are maintaining A&P spend ratios, while shifting spend from price promotion to brand building advertising to defend increased pricing (in an attempt to pass on commodity inflation equivalent to -500bps of margins). In the short term this has been positive for agency revenues, although whether this is sustainable may depend on the extent to which this additional brand investment really does convert into pricing power.

Agency organic revenue growth (quarterly YoY)

Pricing power or post trough bounce?

The issue of pricing power in an inflationary (and possibly stagflationary) environment goes to the heart of of the agency value debate. FMCG clients are shifting spend into branding to support price increases and this is being reflected in agency revenues. Does this mean that we are now entering a new period of above market growth for agencies? I wouldn't bet on it. Marketers may be currently upping their brand spend, but they are also focusing on raising their marketing ROI, including raising the digital mix. Over the past decade this process has dismantled the distribution bottlenecks of many legacy media with the consequential squeeze on advertising yields. If this has resulted in global adverting expenditure growth falling short of GDP, then this has still exceeded agency organic revenues. Hopes that the current growth in marketing investment and agency revenues represents a paradigm shift therefore seems to be wide of the mark. Structurally, legacy media continues to be disintermediated and agency gross margins remain under pressure. Where gains are made in either organic revenue growth or EBITA margins, this often has as much to do with agencies heavy reliance on acquisition to buy new marketing skills and to shed overlapping costs rather than any fundamental evolution in the agency model. If agencies have been spending over two-thirds of their cash flow to acquire skills, one presumes, in faster growth segments, but still deliver organic revenue growth averaging over -100bps pa less than GDP, then what does this really say above their underlying pricing power. While the riposte may be that much of this performance shortfall is recouped by an average +50bps pa of EBITA margin gain, this conveniently ignores any expensing of acquired intangibles which are consumed. Consider the numbers. Even if these intangibles are consumed and amortised over 20 years, this 5% expense on the two-thirds of FCF spent on acquisitions would therefore equate to -3.3% pa of overall FCF, which is just happens to fully absorb the positive benefits of a +50bps pa EBITA margin increase on a 15% margin base. Using the current recovery in expenditure and revenues to justify a resumption of the acquisition led growth model for agencies therefore represents a somewhat bitter-sweet dilemma for the markets, which probably helps explain the muted response to all the positive trading spin we've been getting.

Thursday, 21 April 2011

Publicis Q1 - positive revenue momentum, but is this the real story?

The narrative the markets will focus on will remain the group's ability to translate its digital and emerging market investments into premium revenue growth and further margin progress. From this perspective, Publicis's Q1 revenue performance should be well received. A +6.5% rise in organic revenues pipped Omnicom's +5.2%, reflecting continued progress in digital (+12.6% to 28.2% of revenues) and emerging markets (23.4% of revenues; +1.4pts YoY u/l), while the +58% rise in net new business (to $1.9bn) suggests the service proposition continues to resonate with clients to underpin further relative outperformance. Average net debt meanwhile is down by €500m YoY to only -€100m and the group is sitting on €3.9bn of liquidity, including €2.7bn of committed facilities and €1.7bn of cash and marketable securities.

Markets may focus on the top-line delivery, but the real story should be on what happens to this liquidity. Historically, agencies have applied cashflow to buy new marketing skills to extend their service proposition to clients. This is a great way to build your business and it can also be earnings beneficial as internal investment (thru the P&L) is displaced by acquisition expenditure on intangibles, that loiter in the balance sheet and are broadly ignored in earnings assessments. Markets are not dumb however and recognise that some, or all, of these acquired intangibles are being consumed and discount equity valuations accordingly.

Q1 Revenues

Organic revenue growth of +6.5% vs Q4's +12.8% rate of growth slowed as expected from Q4 spectacular levels (+12.4%), albeit by slightly less than the tightening comparatives might have suggested (Q1 comps at +3.1% were 8pts less favourable than Q4's -5.1%). By region, growth was again driven by

As with other agencies I would expect Publicis's valuation range will continue to be defined by its revenue outlook, which for the moment remains positive. Historically, Publicis has tended to trade at a small discount (on a growth rating basis) to larger agencies, such as WPP and Omnicom, although its current revenue and net business performance may challenge this. At current levels I estimate the shares are discounting trend growth at around 3.5-4.0% pa for 2011 and 2012, possibly dropping to approx +2.5% by 2013. This values the equity at nearer the lower end of what I would regard as a comfortable trading range of +3.5-4.5% and with scope to see this edge up the nearer +5% should the group demonstrate restraint on blowing its balance sheet on an aggressive acquisition spree.

Markets may focus on the top-line delivery, but the real story should be on what happens to this liquidity. Historically, agencies have applied cashflow to buy new marketing skills to extend their service proposition to clients. This is a great way to build your business and it can also be earnings beneficial as internal investment (thru the P&L) is displaced by acquisition expenditure on intangibles, that loiter in the balance sheet and are broadly ignored in earnings assessments. Markets are not dumb however and recognise that some, or all, of these acquired intangibles are being consumed and discount equity valuations accordingly.

Q1 Revenues

Organic revenue growth of +6.5% vs Q4's +12.8% rate of growth slowed as expected from Q4 spectacular levels (+12.4%), albeit by slightly less than the tightening comparatives might have suggested (Q1 comps at +3.1% were 8pts less favourable than Q4's -5.1%). By region, growth was again driven by

- North America: 49% of revenues and +8.1% u/l in Q1 vs +14% in Q4 with digital continuing to provide the key driver to growth.

- Europe: 32% of revenues and +6.2% u/l in Q1 vs +11.3% in Q4 with growth from N and C&E Europe (France +8.2%, Germany >+10%, Russia & CEE +7%, UK +2.4%, but S. Europe trailing)

- LatAm: 5% of revenues and +8.7% in Q1 vs +22.1% in Q4. Declines across Mexico and Columbia partially offset continued strong growth from Brazil and Argentina (>+20%) and Venezuela (>+15%)).

- Asia: 12% of revenues with Q1 at +1.5% vs +6.4% u/l in Q4 as declines across Japan, Australia and Korea substantially absorbed the +8.2% increase from Greater China.

- A&ME: 2% of revenues and -0.5% u/l in Q1 vs +15.3% in Q4. With political unrest sweeping across the Middle East, revenues have unsurprisingly stalled, albeit with some regions still posting growth (UAE +7% u/l).

- BRIC: +11.4%

As with other agencies I would expect Publicis's valuation range will continue to be defined by its revenue outlook, which for the moment remains positive. Historically, Publicis has tended to trade at a small discount (on a growth rating basis) to larger agencies, such as WPP and Omnicom, although its current revenue and net business performance may challenge this. At current levels I estimate the shares are discounting trend growth at around 3.5-4.0% pa for 2011 and 2012, possibly dropping to approx +2.5% by 2013. This values the equity at nearer the lower end of what I would regard as a comfortable trading range of +3.5-4.5% and with scope to see this edge up the nearer +5% should the group demonstrate restraint on blowing its balance sheet on an aggressive acquisition spree.

Valuation

Acquisitions - earnings accretive, but value destructive?

Has anyone noticed that many agencies are currently priced at little more than they have invested in acquisitions over the past decade? For an industry model based on applying cashflow into acquisitions rather than returning to shareholders, this might seem a little embarrassing. When most agencies are also delivering sub-GDP organic revenue growth, despite heavy investments into 'new' growth areas, this might pose a challenge to the whole growth model on which agencies have been based. For Publicis, I estimate that over €9bn has been spent on acquisitions since 1999 (net of disposals and at constant 2010 prices), which is only 13% less the current EV of the group.Acquisitions - earnings accretive, but value destructive?

Equity markets may focus on earnings before amortising these acquired intangibles, but even on this metric, most agencies have also struggled to demonstrate that they have covered their equity cost of capital. While acquisition contributions cannot be disaggregated from the core businesses, one can look at the extent to which real EBITA has risen over the period and then take this against cumulative acquisition expenditure to calculate an implied acquisition ROIC. In the below analysis, I have calculated this on two EBITA growth assumptions of zero and +2% pa at constant prices. On both these criteria, the implied ROIC seems to fall below 8%. While above debt financing costs (and therefore probably EPS accretive on the potion financed with cash), this is below ECC and therefore represents a loss of opportunity value, if nothing else.

Wednesday, 20 April 2011

Omnicom Q1- EPS flattered by FV adjustment

Revenues on track, but FV adjustments flatter margin and EPS beat

While these macro uncertainties persist, consensus revenue and earnings momentum for OMC may well stall for the time being. The shares meanwhile (on these consensus forecasts) appear to have already substantially re-rated to reflect the revenue recovery to date and are discounting growth near the upper end of their historic +3-5% CAGR range. Assuming that we are not facing a double-dip, I would scope a +4-5% CAGR growth rating range for this group and therefore a $40-47 ps price range.

Delivering Q1 EPS of $0.69 vs a consensus expectation of $0.59 ($0.56-$0.63 ranged vs $0.52 for Q1 FY10) seemed like a fairly convincing beat, although the market had not been expecting the $123.4m of book gain from the remeasurement of the fair value of its interests in Clemenger Group, nor the scale of offsetting restructuring charges (of $131.3m, including $92.8m of severance) and nor the accompanying tax benefit which cut 9ppts from the YoY and underlying tax rate (from 34% to 25%). In aggregate these items contributed $19.8m to Q1 net income ($0.07 per share), including -$91.8m/$0.317 ps of restructuring which was clawed back by $120.6m/$0.417 ps of FV adjustments and a -$9.0m/$0.03 ps FIN48 tax accrual.

Without a comparative figure for severance and other restructuring charges that were included in Q1 FY10 it is difficult to draw too many conclusions from the +43bps YoY advance in EBITA margins (to 10.9%). Representing a drop thru rate of under 9% from the Q1 organic revenue growth of +5.2% (vs my +5.1% forecast), this does not seem all that impressive given that Q1 FY10 will have no doubt have included severance charges and while the refilling of bonus pools will have continued to have provided a margin drag into 2011, there should have also have been some compensating cost benefits carrying over from last years cost reductions.

Omnicom EBITA margins & organic revenue growth

Revenues growth continues to define valuation

With net business wins of almost $1.1bn in Q1 ($950m for Q1 FY10) the group remains confident that revenues have now returned to growth in both US (+4.9% and +6.8% excl Chrysler) as well as Internationally (+5.5%, incl >+9% in UK). Prior year comparative however will be progressively hardening throughout the remainder of the year (and by almost 4pts in Q2 vs Q1) and macro uncertainties and moderating GDP expectations (including potential disruptions still to flow thru from Japan) might be expected to provide additional headwinds. For the moment at least, I would expect a neutral to negative forecasting risk to near term consenus revenue growth forecasts.

Omnicom - Organic revenues and growth rating

While these macro uncertainties persist, consensus revenue and earnings momentum for OMC may well stall for the time being. The shares meanwhile (on these consensus forecasts) appear to have already substantially re-rated to reflect the revenue recovery to date and are discounting growth near the upper end of their historic +3-5% CAGR range. Assuming that we are not facing a double-dip, I would scope a +4-5% CAGR growth rating range for this group and therefore a $40-47 ps price range.

Friday, 15 April 2011

Q1 Previews - Agencies

Today's Q1 results from Google provides a prelude to Q1 reporting season for the marketing services groups which kick-off next week (18-22 Apr) with Omnicom which reports on Tues 19th and Publicis on Thurs 21st. The following week IPSOS reports on Tues 27th with WPP and Interpublic on Thurs 28th.

With Q4 recovery momentum already reported to have been maintained into at least the first two months of the Q1 by many of the leading groups, these results will will be scanned more for signs of slowdown into Q2 and the second half of the year as deteriorating macro growth expectations compound the drag from tougher prior year comparatives. While the market's focus will remain on the revenue trajectory, the other feature of note will be any revision to margin expectations and the extent to which the recent uptick in acquisition activity will enable some groups to displace planned internal investment that would have otherwise have diluted this year's margin progression.

Q1 Revenue growth

For the overall sector, I am expecting YoY organic revenue growth to ease back from Q4's +8.9% to just over +5% for Q1 2011, in large part reflecting the increasingly less favourable comparative tailwind as we progress into the current year. After Q4's -6.4% prior year comparative, Q1's hardens to +1.5% while Q2 rises to +5.5% for agency organic revenues. As with the slowing YOY growth rates being reported across a number of media advertising markets such as TV into Q2 as they also cycle through tougher comparatives, we would expect a slightly more cautious tone to adopted by the industry than during the February year end reports, albeit with digital and emerging markets segments remaining strong.

Agency organic revenue growth rates (YoY change)

Not all agencies will report Q1 margins (eg WPP), and for those that do, quarterly margins (and especially those for the thinner first quarter) are usually not that reliable an indicator for the full year anyway. More important will be any change in outlook for the year as a whole. While pricing pressure and pent up cost inflation after the squeeze in 2008 and 2009 will have already have been factored into current year forecasts, competition to invest in new digital services provide an additional potential drag to the pace of margin recovery. For group's such as Gfk which have focused on internal investment (into new measurement and internet services), this could absorb a further 70bps of margin growth in 2011, in addition to the c. 100bps in 2010. Others such as Publicis, WPP and possibly even Havas however are beginning to flex their funding headroom to pursue a more aggressive acquisition strategy, particularly in those areas that might otherwise have been the focus for internal investment. How much of this investment will get shifted off the P&L and into balance sheet intangibles remains a guess, but the sector's record of value creation from acquisitions is poor and also recognised by markets in share prices.

Agency EBITA margins (by key holding group)

Agency sector EBITA margin change and organic revenue growth (YoY change)

Agency organic revenue growth and growth ratings

Subscribe to:

Comments (Atom)